If you own—or are thinking about buying—a home along Alabama’s coast, insurance is no longer a line item you skim past.

For homeowners in Baldwin County, the insurance landscape continues to evolve, and 2026 brings both challenges and clarity.

Understanding how standard hazard insurance differs from wind, hail, and flood coverage isn’t just helpful—it’s essential for budgeting wisely and protecting your investment.

After years of volatility, many buyers ask me the same question: Has the market finally calmed down? The short answer is: it’s steadier than it was, but it’s not cheap.

Let’s break down what’s really happening with Alabama coastal home insurance costs in 2026, and how you can stay ahead of it.

The 2026 Cost Landscape

Premium Trends

The extreme “hard market” we experienced earlier in the decade—when carriers pulled back sharply, and premiums jumped year over year—has eased somewhat.

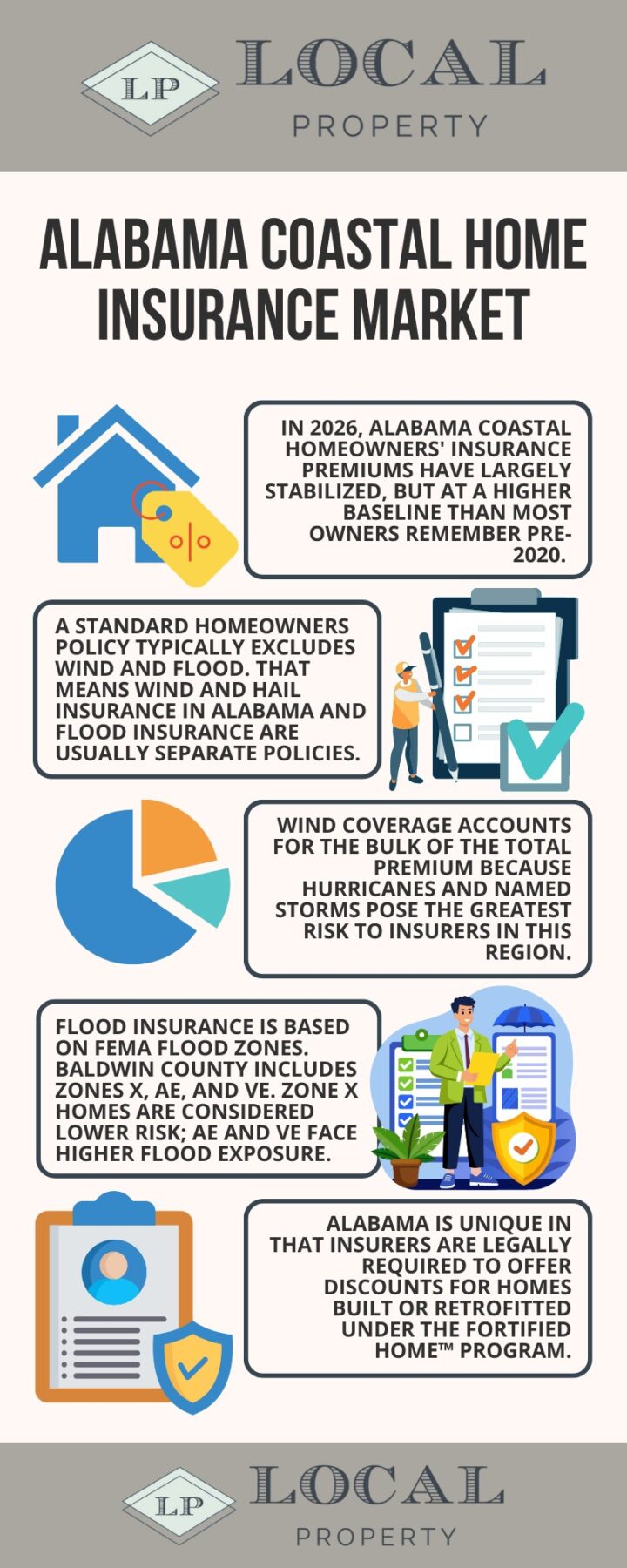

In 2026, Alabama coastal homeowners’ insurance premiums have largely stabilized, but at a higher baseline than most owners remember pre-2020. In other words, rates aren’t skyrocketing like they once were, but they’re not coming back down either.

Cost Factors

Two forces continue to drive pricing.

First, reinsurance costs remain elevated. Insurers along the Gulf Coast rely heavily on global reinsurance markets, and storm exposure keeps those costs high.

Second, construction and material inflation haven’t fully reversed. When it costs more to rebuild a home, it costs more to insure it.

Budgeting Reality

For many coastal homeowners, insurance is now the largest monthly expense after principal and interest.

It’s not unusual for buyers to be surprised when they see how much of their escrow payment is tied to insurance. Going into a real estate purchase with realistic expectations is key.

The Critical Split: Wind, Hail, and Flood

Unbundled Policies

One of the biggest misconceptions I see is buyers assuming one policy covers everything. Along the coast, that’s rarely true.

A standard homeowners policy typically excludes wind and flood. That means wind and hail insurance in Alabama and flood insurance are usually separate policies.

Wind and Hail

In places like Gulf Shores, Orange Beach, and Fort Morgan, wind and hail insurance Gulf Shores is often the most expensive piece of the puzzle.

Wind coverage accounts for the bulk of the total premium because hurricanes and named storms pose the greatest risk to insurers in this region.

Flood Zones

Flood insurance is based on FEMA flood zones, and Baldwin County includes Zones X, AE, and VE. Zone X properties are considered lower risk, while AE and VE face higher flood exposure.

Under FEMA’s Risk Rating 2.0, premiums are now calculated using individual property characteristics—such as distance to water and rebuilding cost—not just elevation. This has made flood insurance more precise, but also more variable from one home to the next.

The FORTIFIED Home™ Advantage

Mandated Discounts

Alabama is unique in that insurers are legally required to offer discounts for homes built or retrofitted under the FORTIFIED Home™ program.

This isn’t a marketing gimmick—it’s one of the few proven ways to reduce Alabama coastal home insurance cost in 2026.

Roof Certifications

A FORTIFIED Roof is the most impactful upgrade. Depending on the level—Bronze, Silver, or Gold—homeowners often see a 20% to 50% reduction on the wind portion of their premium.

From an ROI standpoint, no other improvement comes close for coastal properties.

Understanding the Wind Pool (AIUA)

The Safety Net

The Alabama Insurance Underwriting Association (AIUA), commonly called the Wind Pool, exists for properties that private insurers won’t cover.

It ensures that homeowners can still obtain wind coverage when the private market declines them.

Coverage Limits

The Wind Pool can be a lifeline, but it comes with trade-offs. Coverage limits may be lower, and premiums are often higher than private-market options.

Whenever possible, securing private wind coverage is preferable—but the Wind Pool remains a crucial backstop.

Strategic Deductibles and Coverage

Hurricane Deductibles

Unlike standard deductibles, hurricane deductibles are usually calculated as a percentage of the insured value—commonly 2%, 5%, or even 10%. On a $600,000 home, a 5% deductible means $30,000 out of pocket before coverage kicks in.

Self-Insurance Risk

Higher deductibles can significantly reduce annual premiums, but they shift more risk to the homeowner. Choosing the right deductible is about balancing cash reserves with long-term savings.

Frequently Asked Questions

Costs vary widely, but many homeowners see annual premiums ranging from the high four figures to five figures, depending on construction, roof age, and proximity to the water.

No. The roof must meet specific installation standards and be certified through the FORTIFIED program.

In some cases, yes. Policy assumptions are allowed, but eligibility depends on the insurer and the property’s current risk rating.

Eligibility is typically determined after private carriers decline coverage. Your insurance agent can guide you through the process.

It’s not federally required in Zone X, but many lenders still recommend it, and the cost is often relatively modest.

HO-3 policies provide named-peril coverage for contents, while HO-5 policies offer broader open-peril coverage. Availability varies by carrier along the coast.

Roof certifications typically need to be renewed every five years to maintain insurance discounts.

Key Takeaway

Resilience Pays. In the 2026 market, the most reliable way to manage long-term Alabama coastal homeowners’ insurance costs is resilience.

Homes with FORTIFIED designations consistently outperform others when it comes to premiums.

If a property isn’t already upgraded, budgeting for immediate improvements—especially the roof—can make the difference between manageable costs and ongoing frustration.

If you’re buying, selling, or simply reviewing your Alabama coastal home insurance strategy, it pays to get expert guidance before making decisions that could cost thousands down the line.

I can help you navigate wind and hail insurance, flood policies, deductibles, and the FORTIFIED Home™ program so you can make informed choices for your property.

Reach out today at (251) 270-6400 or via email at hollie@localpropertyinc.com, and let’s make sure your coastal home is properly protected without breaking the bank.